Why is Crypto so Volatile?

Why is Crypto so Volatile?

Magic Internet Money's Minsky Moments...

Minsky Moments & the Lender of Last Resort

In today’s “macro-heavy” world, one paradigm I have found helpful - particularly in crypto - is the Minsky moment. A close cousin to Soros’ Theory of Reflexivity, Minsky was a post-Keynesian American economist who preached the endogenous nature of the market cycle.

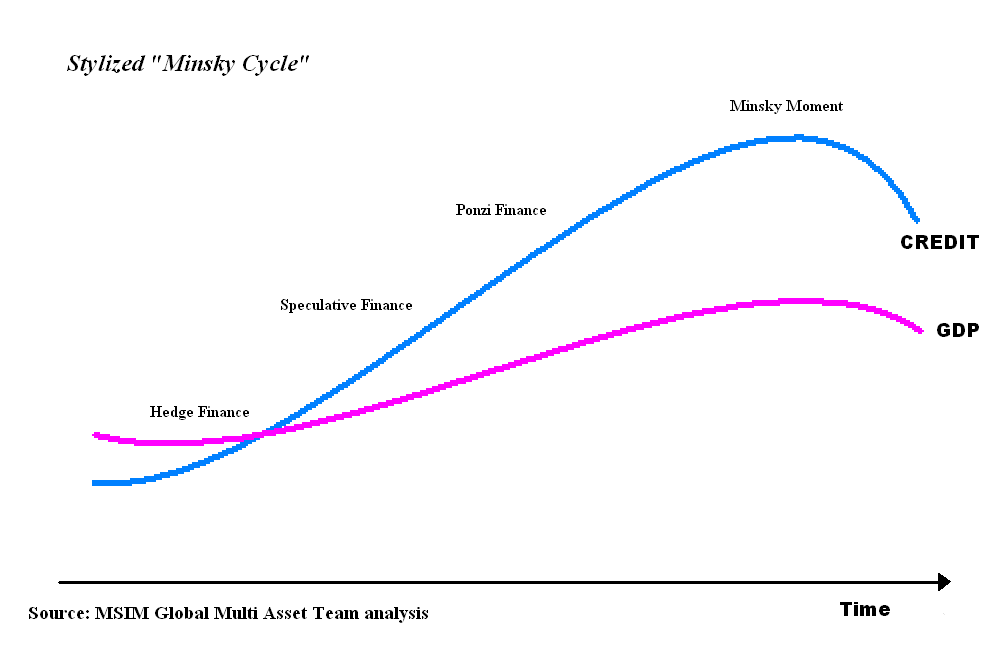

A Minsky moment is a sudden collapse of asset values, typically following a long period of asset price inflation and overvaluation. Long periods of stability and prosperity often lead to greater risk-taking and leverage. This investor complacency is followed by a sudden collapse in asset prices, causing the prior buildup to unwind quickly, leaving behind cascading defaults and liquidity crises which can spill over into the “real economy”.

Despite technocratic narratives of “taming the business cycle”, suppressing human nature has proven evasive:

The reinforcement between increasing asset values and growing risk-appetites, causes the pace of borrowing to outrun underlying productivity growth.

Eventually a catalyst (often a tightening of financial conditions), will cause market participants to take some chips off the table. The credit cycle then kicks into reverse…

The Minsky Moment:

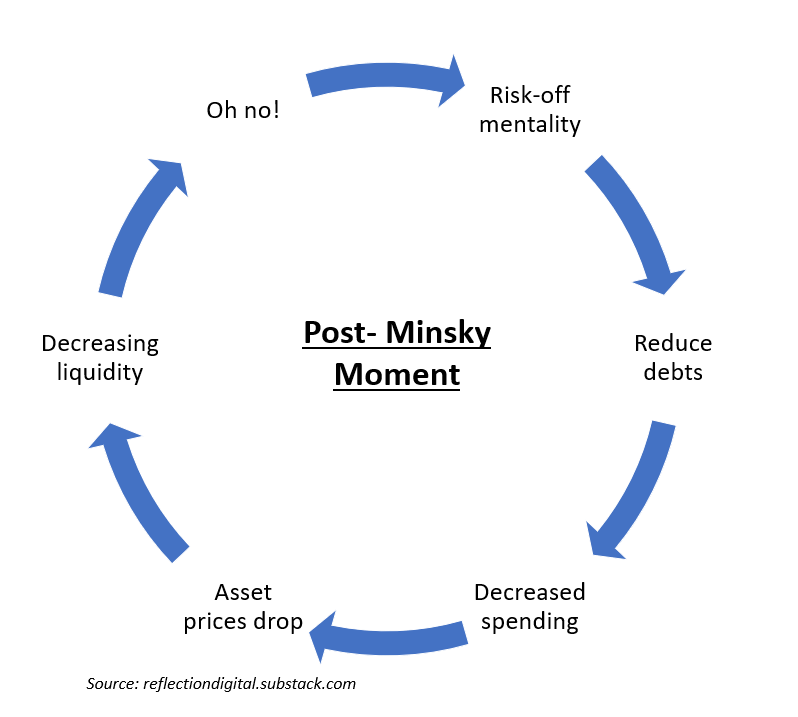

The deleveraging is typically much faster than the initial run up. Margin calls force selling and asset price decreases force margin calls in a mutually-reinforcing unwind, all against a backdrop of vanishing liquidity. The wealth effect evaporates; low consumer spending seeps into earnings further weighing on asset prices which can flow into unemployment figures as management “right sizes” the cost structure.

Monetary policy is often a central driver, the expansion or contraction of M2 into the financial system is a key ingredient to both the build up and the unwind. Minsky, like Keynes, was in favor of government intervention to stem the deflationary collapse - not letting the excesses of financialization spill over into underlying economic productivity.

***Skip to the footnotes now for an overly detailed exploration of the theoretical tug-off-war between neo-classical and Keynesian technocrats which drove the monetary policy pendulum during the last 100 years which I ultimately decided was nothing more than a fun detour... ***1. For the normies, please read on....

Minsky’s writing’s went largely under-explored until 2008 when the neo-liberal consensus shattered spectacularly; years of near-blind underwriting which led to the world’s largest Minsky moment since the Great Depression: the subprime mortgage crisis. The reigns were once again handed back to Bernanke and the Keynesian camp, electing for massive rounds of quantitative easing to counter-act the deflationary implosion of one of the world’s largest asset classes.

In the aftermath, however, we are having a hard time weening off the medicine. Monetary and fiscal restraint is out of vogue on both the right and the left, with deficits climbing regardless of who is in power.

While government counter-cyclical intervention is a helpful tool to stave off harmful unwinds after a Minsky moment, if abused, it can simply push short-term private market volatility into systemic fragility at the base layer: government finances.

It certainly seems like trading short-term volatility for a larger Minsky moment in the future. Interestingly, crypto’s libertarian experiment was birthed in protest to this exact moral hazard, hoping to provide an alternative:

A parallel financial system based on the promise of transparency, immutability, and distributed, algorithmic monetary policy. Frustratingly, from the vantage point of 2022, reality has dramatically under-performed the vision.

Where did it go wrong?

Why is Crypto So Volatile?

In 2022, crypto has been plagued by a slew of very public hacks, frauds, and bankruptcy’s leaving a trail of scandals and scarred speculators in its wake.

The grandiose promises of web3 - A replacement for a broken financial system? A counter-balance to the growing market power of the data monopolies? An escape from the looming financial repression of national governments? - reduced to a pile of lawsuits, squandered funds, and what certainly looks like nothing more than the burning ruins of a leverage-filled casino of “pet rocks”.

Outside of the DeFi “rugs” and even more so the irresponsible / illegal behavior of many centralized companies in the space (which cannot be justified), the number one complaint is:

“Why is it so volatile?”

How can an 80+ vol asset class be a “store of value” or a “medium of exchange” or a “unit of account” underpinning a new financial system?

A fair point. Since the movement’s birth in 2009, the asset class has undergone three drawdowns >80%. The post-Minsky corrections in crypto are apocalyptic relative to the existing system. But why? Will this ever change?

Below is my list of the underlying drivers of crypto’s volatility. Some points the movement will outgrow, but others are more endogenous to a completely open system, which is difficult to regulate, and does not have a fluctuating monetary base which absorbs the volatility of the traditional system.

Immature “call option” stage of market development

Crypto is still in its early innings. The technology has large potential, but remains unproven. It’s “venture risk, with public market liquidity” naturally leading to more volatile swings as the probabilities impacting crypto’s more distant future unfold today. A “call-option” on becoming “digital gold” or the future “decentralized operating system” have real adoption and execution risk which must be discounted back to the present at high rates.

Limited regulatory oversight

Excessive leverage, market manipulation, and fraudulent behavior are fairly endemic in today’s crypto market. While often excessive, securities laws and regulatory compliance stamp out the most blatant of malfeasance. Regular DeFi “rugs”, ~100x leverage offered to market participants, and insider pump and dumps clearly add to market volatility in this “buyer beware” financial free-for-all. While sometimes heavy-handed, we should not pretend regulation does not have benefits.

The massive build up of leverage in particular, both collateralized and undercollateralized to suspect actors has clearly had an impact on the violent Minsky cascades we have witnessed in 2018 and 2022.

Retail-heavy, global asset class in the social media era

Given its immaturity and size, digital assets still have not reached widespread institutional adoption leaving it captive to “hot money” flows without institutional anchors. Crypto-native traders tend to favor momentum, with leverage. Social media platforms like Twitter, Tiktok and Reddit further boost asset class reflexivity correlating market sentiment in a system accessible by anyone with an internet connection.

Limited “Fundamental Value” in the traditional sense

Layer 1 protocols are more like commodities than equities and so marginal supply / demand can lead to wide swings in price. The application layer of crypto systems is still immature and trades like unprofitable growth-stage tech - spiking and falling in line with interest rates and liquidity conditions with limited cashflows to underpin “floor” valuations.

No lender of last resort

Lastly, crypto does not benefit from the counter-balancing flows of a central backstop. The Minsky moment is left to its own devices in an asset class suffering from the four preceding volatility enhancers. Today, crypto remains a libertarian experiment, subject to the swings of global, unregulated, levered liquidity flows. When sentiment turns, the positive build up unwinds completely, with nothing to cushion the fall.

While highly imperfect, the interesting question becomes: would you rather have a highly volatile system with greater long term resiliency or a system which smooths out near-term volatility at the expense of systemic fragility? Unfortunately, the optimal blend of the two has proven evasive.

In that sense, there is something healthy in crypto’s regular track-record of completely wiping out speculators and irresponsible actors absent moral hazard. However, this habitual cleansing remains something crypto market participants should always remain cognizant.

I have noticed crypto veterans in their second or third cycle tend to be the most cautious. The scars from 2014 and 2018 are still fresh. Many flee to stables at the first sign of trouble, knowing from experience that leverage can disappear in an instant.

For those planning to stick around in the asset class for the next re-leveraging (which I highly recommend), let’s try to remain vigilant. In 2024, when the good times return, when “#super-cycle” is trending, “laser eyes” stage a comeback, and leverage loops are once again in vogue, please keep Hyman in mind. As long as the five attributes above remain, a Minsky moment is always just around the corner.

In crypto, there is no one to cushion the fall.

***

Merry Christmas :)

Hayek, Keynes, Friedman, Bernanke & the Lender of Last Resort

Today, it’s a consensus belief central banks and governments can shorten recessions by providing counter-cyclical liquidity injections to stave off deflationary spirals. Technocratic mandarins fine-tuning the dials to course correct from market inadequacies. Yes, “we are all Keynesian’s now”. However, this consensus is a fairly recent phenomenon; the economic tides of pro-interventionist policies ebbing and flowing substantially over the last 100 years.

Keynes rose to the pantheon of economic greats following his publishing of The General Theory in 1936 in the doldrums of the Great Depression. The decade long deflationary slump had pushed Friedrich Hayek’s Austrian camp stage right, convincing many economists that markets were in fact fallible. They did not always snap back to equilibrium, unemployment could be sticky, competition imperfect, and government intervention an important tool to get markets “unstuck”.

The new doctrine reigned supreme from the 40s - 60s, a generation of policy makers nourished on the sweet nectar of Keynesian intervention to smooth out certain market inequities and inefficiencies. However, during Minsky’s prime, the tide reversed course.

Minsky’s most famous paper’s “The Financial Hypothesis” (1972), “The Analysis of Financial Instability: An Introduction” (1986) and “The Financial Instability Hypothesis (1992)” were written in the face of the 70s rising stagflation which preceded Reagan’s and Thatcher’s neoliberal turn. The Chicago School led by Milton Freidman won the day: government intervention was the problem, markets the solution. With the changing tides, Minsky’s writing largely went uncelebrated…

Until 2008.

The 2008 financial crisis was arguably one of the largest Minsky moment’s in history: a dizzying build up of subprime credit in one of the world’s largest asset classes underpinned by an orgy of irresponsible underwriting predicated on the belief housing prices could only go up…

The market once again proved fallible. In a massive way.

The pendulum swung back in a hurry. Ben Bernanke - a student of the Great Depression - opted for a Keynesian prescription to prop up aggregate demand to stave off the deflationary onslaught. While the counter-factual is impossible to ascertain, Bernanke almost certainly postponed significant economic pain, allowing for a still slow, but likely meaningfully shortened recovery from the largest Minsky moment since 1929.

Fourteen years later, we have arguably over-rotated once again; the correct balance between government intervention and fiscal discipline has proven elusive. Since 2008, central bank balance sheets around the globe have ballooned, injecting ever greater quantities of debt in exchange for disappointing growth rates.

Ok… back to the main text…